The U.S. economy shrank at a 0.5% annual pace from January through March as President Donald Trump’s import taxes at least temporarily disrupted business, the Commerce Department reported Thursday in…

WASHINGTON (AP) — The U.S. economy shrank at a 0.5% annual pace from January through March as President Donald Trump’s trade wars disrupted business, the Commerce Department reported Thursday in an unexpected deterioration of earlier estimates.

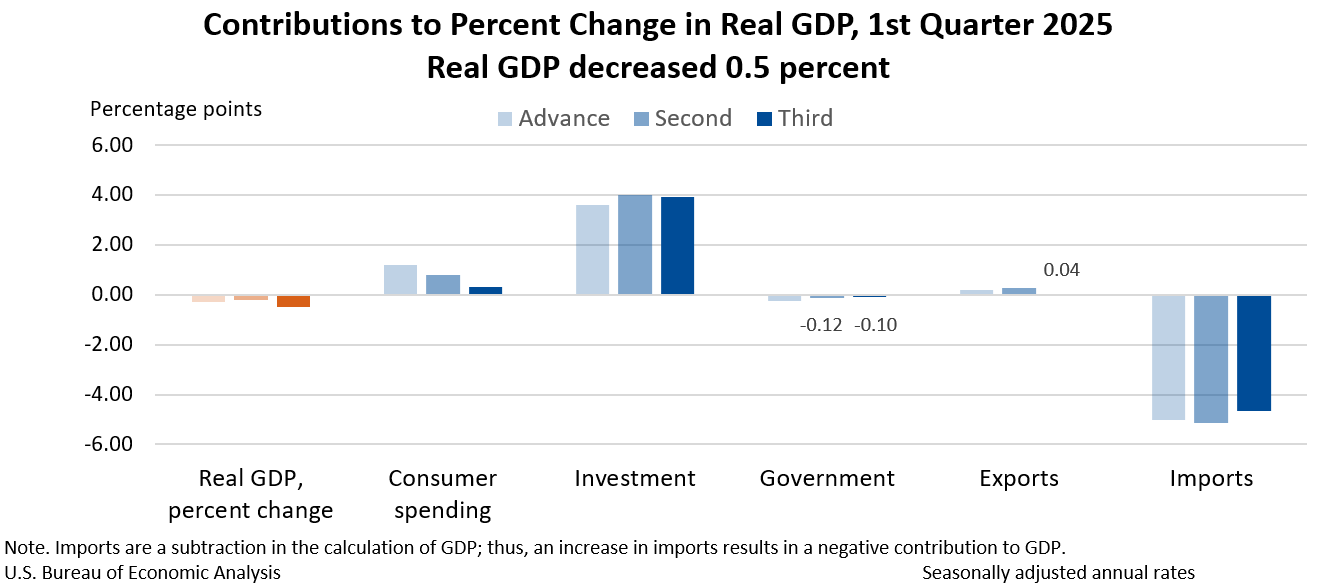

First-quarter growth was weighed down by a surge of imports as U.S. companies, and households, rushed to buy foreign goods before Trump could impose tariffs on them. The Commerce Department previously estimated that the economy fell 0.2% in the first quarter. Economists had forecast no change in the department’s third and final estimate.

The January-March drop in gross domestic product — the nation’s output of goods and services — reversed a 2.4% increase in the last three months of 2024 and marked the first time in three years that the economy contracted. Imports expanded 37.9%, fastest since 2020, and pushed GDP down by nearly 4.7 percentage points.

Consumer spending also slowed sharply, expanding just 0.5%, down from a robust 4% in the fourth-quarter of last year. It is a significant downgrade from the Commerce Department’s previous estimate.

Consumers have turned jittery since Trump started plastering big taxes on imports, anticipating that the tariffs will impact their finances directly.

And the Conference Board reported this week that Americans’ view of the U.S. economy worsened in June, resuming a downward slide that had dragged consumer confidence in April to its lowest level since the COVID-19 pandemic five years ago.

The Conference Board said Tuesday that its consumer confidence index slid to 93 in June, down 5.4 points from 98.4 last month. A measure of Americans’ short-term expectations for their income, business conditions and the job market fell 4.6 points to 69. That’s well below 80, the marker that can signal a recession ahead.

Former Federal Reserve economist Claudia Sahm said “the downward revision to consumer spending today is a potential red flag.’' Sahm, now chief economist at New Century Advisors, noted that Commerce downgraded spending on recreation services and foreign travel — which could have reflect ”great consumer pessimism and uncertainty.’'

A category within the GDP data that measures the economy’s underlying strength rose at a 1.9% annual rate from January through March. It’s a decent number, but down from 2.9% in the fourth quarter of 2024 and from the Commerce Department’s previous estimate of 2.5% January-March growth.

This category includes consumer spending and private investment but excludes volatile items like exports, inventories and government spending.

And federal government spending fell at a 4.6% annual pace, the biggest drop since 2022.

In another sign that Trump’s policies are disrupting trade,

Trade deficits reduce GDP. But that’s just a matter of mathematics. GDP is supposed to count only what’s produced domestically, not stuff that comes in from abroad. So imports — which show up in the GDP report as consumer spending or business investment — have to be subtracted out to keep them from artificially inflating domestic production.

The first-quarter import influx likely won’t be repeated in the April-June quarter and therefore shouldn’t weigh on GDP. In fact, economists expect second-quarter growth to bounce back to 3% in the second quarter, according to a survey of forecasters by the data firm FactSet.

The first look at April-June GDP growth is due July 30.

____

This story has been corrected to show that the drop in federal spending was the biggest since 2022, not 1986.

Read the original article

Comments

I'm a bit confused about the bit about the "Imports expanded 37.9%, fastest since 2020, and pushed GDP down by nearly 4.7 percentage points" bit.

Presumably when they calculated GDP previously, they hadn't seen quite as much imports, but had seen higher spending, thus they misattributed some of it to domestic products rather than imports, though I'm a bit confused as to how they underestimated imports given everything is declared. Perhaps some changes in the price index?

Though other articles talk about the expected GDP next quarter being higher because they don't expect a surge of imports to continue, which makes no sense to me unless one assumes spending remains the same with or without imports.

By iamtheworstdev 2025-06-2620:067 reply stolen from investopedia: The GDP formula is commonly expressed as GDP = C + I + G + (X - M), where C is consumer spending, I is business investment, G is government spending, and (X - M) represents net exports (exports minus imports). This formula helps measure the total economic output of a country during a specific period.

Our tariffs are tampering with the intelligent monitoring of GDP growth. When the USA expanded tariffs to 155% with China it was effectively an embargo, so imports went away (but exports didn't) and our GDP looked amazing. When the tariffs were brought back to previous rates of 55%, companies bought every import they could (or had them released from bonded warehouses) which has pumped the GDP in the other direction. And it'll likely be the same situation next month because Chinese ports are seeing record numbers as US companies try to buy every piece of inventory they can before these tariffs go back up.

One of the most upsetting things about our current state of governance is gamed metrics and lack of a national metrics "dashboard."

Metrics are gamed as marketing tools rather than assessment tools. There's a clear conflict of interest in the government presenting the metrics that it says to judge them by.

Unemployment is another gamed metric. If you want to get a sense of unemployment, a graph of % employed tells you more than some gamed number like "unemployment" since "unemployment" is a direct measure of political success.

Consumer spending/GDP are also directly used to measure political success, and a metric like "aggregate Visa/Mastercard purchases" is going to give a much better sense of how much people are spending.

During COVID, all cause mortality is a superior metric than COVID attributed deaths because any death attributed to COVID represented a failure of public health policy. We even saw direct attacks on public health monitoring in Florida.

It seems like the only ways to combat this are either states presenting their own metrics to imply national trends based on their own. I definitely wonder what kind of information we could get that is accurate and not gamed to create our own dashboards. Geohot's use of national energy consumption to estimate national productivity was sharp and the type of thing I wish journalists would do.

I don't think you know the space very well. Go to FRED, it is the largest of many that is a fantastic unbiased dashboard of governmental and societal data for the US. They even have almost the exact data that you would say is useful about CC spending. Here is all of the data that they publish about credit cards[1]. It has a lot more data than just the aggregate data from two of the credit card providers.

The people that gather and publish the data are historically pretty unbiased and open about methods. You can go get the raw data and methods. Some of the places that publish them like FRED, are not even under direct political jurisdiction. They are not at all the part of the government that is affected by the data they publish, and being run by a reserve bank puts them at pretty far reach from meddling by DC.

You can't stop politicians from using the data they like most, but don't pretend that ALL of the data isn't available in useful format.

By sillyfluke 2025-06-270:531 reply >being run by a reserve bank puts them at pretty far reach from meddling by DC.

Study the path other autocrats blazed for Trump, who is following and mimicing their tactics pretty closely now. Aggressive Fed interference is on his agenda, as can be seen by the way he likes to keep his fights with Powell constantly in the news cycle.

By dghlsakjg 2025-06-271:52 Well aware.

At least the few adults that are left, along with the market, start getting very upset when certain politicians target the fed.

By TheOtherHobbes 2025-06-2623:573 reply It's not the data, it's the media narrative. No one cares if there are detailed breakouts of key economic indicators available somewhere obscure [1] if most people get their opinions from the media, and the media are in the propaganda and marketing business, not the truth-to-power business.

[1] Not media-quoted or foregrounded for the public.

That's a goal-post shift. GP were complaining that accurate, fulsome statistics aren't there, when they are.

The media narrative is out of the control of the various statistics bodies, and it is up to the informed reader to seek out better sources if the article they are reading has scanty info. For the record though, FRED is frequently cited as a source in reputable mainstream media (I see it in the NYT all the time). Read The Economist some time, that's an international news source that will deeply report on these stats. Can't be helped if people prefer Fox or other garbage as their news diet.

You are complaining about media literacy and bad journalism, which is an entirely separate issue from the fact that the data both exists, and is extremely easy to access.

By firesteelrain 2025-06-273:071 reply It feels like both things can be true at once: the raw data is often accessible and methodologically sound (shoutout to FRED, BEA, BLS, etc), and the interpretation or prioritization of metrics by politicians and media can completely skew public understanding.

The frustration isn’t about access it is about trust.

People want metrics that reflect lived reality and can’t be spun or redefined every election cycle.

Except that mainstream media do use FRED data ... so.

It is also possible to try to paint journalists as worst then they are ... that is good for actual quacks that to not like the good data.

By firesteelrain 2025-06-2710:14 I never said journalists don’t use FRED. The issue is which metrics get foregrounded and how they’re framed. The data’s out there, but the signal-to-noise ratio in most news cycles is terrible.

By trainerxr50 2025-06-2712:22 The irony is that is is a more fundamental problem that both of us are engaged in right now.

Why are we wasting our time having this discussion and not just debating the finer points of Wittgenstein?

Once basic needs are met humans mostly do things for fun and entertainment. Truth seeking is mostly an after the fact justification for what was fun and entertaining in the moment.

Sich meinen, einer regel zu folgen, ist nicht, einer regel folgen.

By datavirtue 2025-06-271:35 You are supposed to be an adult and ignore all that biased rhetoric.

By trainerxr50 2025-06-2712:081 reply Exactly. It is like when people complain about the inflation rate not reflecting reality but of course haven't bothered to look at the FRED data and how incredibly granular they do go with the data. Really not even understanding that the inflation rate is an index.

As if you can go more granular than Producer Price Index by Commodity: Chemicals and Allied Products: Thermoplastic Resins and Plastics Materials https://fred.stlouisfed.org/series/WPU0662

It is like with GDP and unemployment. These are incredibly hard things to measure at the scale of the US economy. How can a thinking person not understand this is beyond me.

By wjnc 2025-06-2718:46 “ How can a thinking person not understand this is beyond me.”

Measurement theory is not a subject taught pretty much anywhere? I have a masters in economics and the only reason I have more than an inkling of understanding of these things is via an internship at our nations statistical bureau.

You get taught to think With numbers. Thinking About numbers is pretty special! Physics, econometrics, abstract math, statistics - they force you to think About numbers. The rest is thinking With numbers.

By rrrrrrrrrrrryan 2025-06-2621:31 Politicians brag about the U-3 unemployment (that they've gamed), but actual economists look at U-6 (unless they need to do a comparison going back a century, when U-6 didn't yet exist).

During covid politicians bragged about covid attributed deaths, while public health experts were discussing all cause mortality.

This is the case everywhere. Quality metrics are absolutely out there - you just have to give enough of a shit to look at them.

By kasey_junk 2025-06-2623:05 GDP, consumer spending, unemployment are some of the most inspected numbers in the world. Not only are they rigorously defined and tested by the government and academia there are whole swaths of finance attuned to them.

And no one who uses them seriously doesn’t understand their weaknesses. At a macro level all signals have flaws, knowing what they are and how to deal with them is the whole job of many people.

You can find huge swaths of research comparing and contrasting the ADP number vs the official bls stat but no one serious thinks ADP is _better_ than the the headline unemployment number because it can’t be gamed.

By jaredklewis 2025-06-283:05 Marketing for the government? Only a tiny sliver of the population gives these metrics any thought. Certainly politicians don’t.

Econometrics is a political loser; culture wars and other qualitative arguments decide elections. When politicians do bring out numbers, they cherry pick dramatic examples like the price of eggs, not meaningful stuff like CPI or GDP.

By mensetmanusman 2025-06-2713:19 Every metric is a lossy compression algorithm of reality:

“”Unemployment is another gamed metric. If you want to get a sense of unemployment, a graph of % employed tells you more than some gamed number like "unemployment" since "unemployment" is a direct measure of political success.””

Even in this case, you may have to normalize to the population pyramid that is inverting because the age is shifting to much older than prior.

By protocolture 2025-06-2623:41 >Metrics are gamed as marketing tools rather than assessment tools.

Macro metrics are marketing tools largely.

In Australia we had a long period of "Lower Taxes" Vs "Lower Taxes (As a proportion of GDP)" The issue being that the latter didnt actually lower taxes, they just spent more money, increasing GDP.

These metrics are helpful sometimes in review. But in terms of targets they suck.

By datavirtue 2025-06-271:34 The calculations are 100% transparent. Reminds me of the red hat crowd bleeting about how the numbers are "adjusted." Like it's some kind of conspiracy. It's all well known. If you understand it and choose not to like it, well ignore it and cook up your own stat. You can find the formulas and get the data. No secrets.

By randomNumber7 2025-06-2622:16 So you are in favor of temporally changing the GDP formula to fit your mindset better?

From what I understand from Econ 101, this is not true. The only reason you subtract imports is to avoid double counting because presumably the import was done by C, G or I.

The point of subtracting imports is so that it doesn't count as domestic production, and effectively zeros out the portion of C + G + I that was not produced domestically, but thats independent of how much is in exports.

By digitalPhonix 2025-06-2621:432 reply That’s true (analogy - you can find out how much the clothes you’re wearing weigh by weighing each piece individually or weighing yourself wearing them and subtracting your weight).

But you can’t change the process mid way through your measurement. We don’t have a way of measuring “consumption of domestic products” so we just measure consumption and subtract the imports afterwards.

X-M is an accounting trick, but when you’re using this model you have to stick with it.

The idea that imports were deferred causes this accounting trick to show its weakness. (Presumably, looking at the data for all of 2025 when it’s available will “low pass” the deferred imports)

I'm not sure I understand. What process is changing? The "accounting trick" doesn't stop working.

Let's try a very simple example of buying all our inventory in one quarter and selling it in another - what is supposedly behind our GDP woes.

Let's say in Q1, the only spending was on $1 trillion of imports into private inventories, thus: I=$1 trillion, C=$0, G=$0, X=$0, M=$1 trillion. That gives us a GDP of $0.

Next quarter, flush with product there's no need to import anymore and the entire inventory is somehow sold domestically, thus: I=-$1 trillion, C=$1 trillion, G=$0, X=$0, M=$0. That gives us again, a GDP of $0.

Yet articles claim that the GDP in Q2 would be higher due to the drop in imports and was reduced in Q1 due to an increase in imports.

Don't you always measure GDP using spending (for convince / accuracy of price) so if you import $1 trillion and don't sell it then the GDP is $-1 trillion?

So Q1 is $-1 trillion and Q2 is $1 trillion?

IIRC, Investment is more of I bought machinery to make socks not I have 100 nintendo switches.

By Aloisius 2025-06-2623:26 I (investment) in the GDP includes changes in private inventory, not just spending on fixed assets, so the 100 nintendo switches should be in there.

That's why in my example Q2 investment goes negative since inventories get depleted when they are sold.

By dylan604 2025-06-2622:16 > (analogy - you can find out how much the clothes you’re wearing weigh by weighing each piece individually or weighing yourself wearing them and subtracting your weight)

damn, my clothes are heavy, because I know how much I weigh.

By Aurornis 2025-06-2623:43 > The GDP formula is commonly expressed as GDP = C + I + G + (X - M), where C is consumer spending, I is business investment, G is government spending, and (X - M) represents net exports (exports minus imports).

Imports don't actually subtract from GDP. They are subtracted inside the GDP formula to make sure they aren't counted toward the country's production, basically.

Logically it makes sense: If you import something, it was not produced within the country. Therefore you need to make sure it's not counted in GDP. However, the starting values for GDP calculation are sum total type numbers, so you have to manually subtract out imports.

This proves endlessly confusing for journalists and even politicians who see the subtraction sign and conclude that "imports subtract from GDP"

Chris Clarke has a great Short on this: https://www.youtube.com/shorts/UrsRoHmXCug

In a non-terrible format: https://www.youtube.com/watch?v=UrsRoHmXCug

how is that better? the selected background color is not better than black which is what most players will do when forced to a landscape player

That seems very strange to me that GDP is the same, when import:export is 4:3 or 3:2, but explains why someone would care more about the difference than the absolute values.

By notahacker 2025-06-2620:59 They're accounting identities, not casual relationships. Exports are stuff that's part of domestic product (but not consumed domestically) so get added. Imports are stuff domestic consumers get the benefit of but aren't actually produced domestically, hence the direction of the signs in the accounting identity. The 4:3 ratio is consistent with an economy which might be more open than a 3:2 one, but it doesn't actually have a higher GDP unless there's higher consumption or investment or government spending as a result of the extra trade.

The key part is that nobody should care about any values or ratios in isolation or impute causality that isn't there. Otherwise people start believing that doing crazy stuff to shrink a trade deficit results in higher GDP, as opposed to lower C+I+G. And when those people are sufficiently stubborn and sufficiently powerful, you get $economy shrank 0.5% in the first quarter headlines...

By yread 2025-06-2620:58 If you import something and immediately export it the ratio changes but the difference doesnt

By gowld 2025-06-2621:33 Quarterly GDP, since it's measured via global approximation, isn't meaningful in quarters when the economy is rapidly changing. The numbers only make sense over time periods where behavior is relatively steady.

Spending did not keep up; if it had, the net effect on GDP would be zero.

This is companies stocking up, and the items are in inventory. They will sell it over the next quarter or so, at which point the tariffs will really weigh.

By cchance 2025-06-2621:11 I've heard this from a number of buyers for companies, that their companies have hugely held stockpiles, to avoid the tariff uncertainty in hope they get worked out before stockpiles run out... most of the ones i've talked to say its only gonna last a few months before shit really hits the fan

By outside1234 2025-06-2619:582 reply My theory would be that a lot of companies imported a ton in the first quarter knowing that tariffs were coming.

By Espressosaurus 2025-06-2620:001 reply My company did that. Along with rushed some deliveries that weren't 100% ready to avoid the sudden spike in tariffs.

I also personally did that for expensive gear I was otherwise planning on waiting on. And now I'm not going to be buying that over the next 2-5 years like I was originally planning.

It's a big bolus of spending that will not be replicated in the future.

By don_neufeld 2025-06-2620:45 Yup, did the same, ton of new hardware.

Last week I was looking at a proposal from a supplier that's got a ~8K "tariff" line on it and thinking... y'know, I can wait on that project.

By WaxProlix 2025-06-2619:59 Sure, but GP's point is that that level of spending likely won't continue now that the (forecasted) demand has been met.

By Matticus_Rex 2025-06-2621:03 In the quoted statement, they're reasoning from an accounting identity because they don't understand the underlying measure. There's a kernel of truth, but it's much more complicated than that.

Imports are subtracted from the GDP calculation, BUT, that's only because they're added in the equation as well as part of consumption/investment/government spending. So to capture only the domestic production, since it's hard to measure consumption/investment/government spending only on domestic inputs, you just measure them overall, add exports, and subtract imports.

So people see that in the equation imports are literally subtracted as a variable, and reason that if imports go up $X, that means GDP literally goes down by that amount. In reality — ignoring for a moment that we sometimes mismeasure consumption/investment/government spending, the net effect in the equation is 0.

ON THE OTHER HAND, in one way part of the GDP drop here is because of imports. It's not something you can cleanly calculate the way journalists often try to, because there's a lot we don't know, but picture this simplified example:

I'm a factory owner, and my factory uses a lot of inputs that we import from China. We normally spend $50k/quarter on investment (maintenance, new machines, etc.). But next quarter my short-term cost of Chinese inputs may double. It may make sense for me to front-load imports ahead of tariffs and defer as much investment as possible. I can't do that forever, so eventually the money will show up in the equation more-or-less where it would have otherwise.

And on top of that, there are a bunch of confounding factors. Over time, imports also make domestic production more efficient, so shifting to less-efficient US inputs (or simply paying the tariff) will slow the rate of overall growth. And some costs are passed on as higher prices, which reduces demand, and therefore reduces growth. And importing goods also means exporting dollars, which affects exchange rates, and therefore affects exports as well. It's all interconnected.

Calling it out when they reason from an accounting identity is really important, because it's a lot of what drives the misconceptions of Trump's protectionist advisors — they use the same reasoning in reverse to say that anything that reduces the trade deficit therefore increases GDP. But that's only true in an accounting sense! Reality takes more complex modeling, and has to account for all the interconnected pieces.

By ACow_Adonis 2025-06-2622:262 reply See this article: Why do econ journalists keep making this basic mistake.

https://www.noahpinion.blog/p/why-do-econ-journalists-keep-m...

Source: am economist, and the writer of the blog is 100% correct.

Reporting and commentary on GDP and economics stats is just generally bad.

By Aloisius 2025-06-2623:54 Thank you. This makes far more sense.

By neilwilson 2025-06-275:45 However Economists tend to struggle with flow effects, and Noah is no exception.

Trade deficits are exports of money as static savings, and that reduces money in flow within the USD currency area. Deliberately, as that is how neo-mercantalism operates. The impact is on the income/expenditure sequence, not the aggregate figures - which are massaged by the reporting currency effect.

By RC_ITR 2025-06-2620:27 Preamble: GDP, is a bit of a synthetic metric.

As you point out, there's no purchase level data about what's imported vs. not.

The way this is handled is that this quarter's imports are set against this quarter's consumption - basically the method assumes the import/domestic mix of business inventories stays the same (true enough in the long run, very incorrect in short term shocks).

That's why extremely disingenuously the AP says:

>Trade deficits reduce GDP. But that’s just a matter of mathematics. GDP is supposed to count only what’s produced domestically, not stuff that comes in from abroad. So imports — which show up in the GDP report as consumer spending or business investment — have to be subtracted out to keep them from artificially inflating domestic production.

Answer: What happened here[1] is that the BLS makes a bunch of assumptions to get data out in time (preliminary figures based on historical seasonal trends, etc.) but this quarter, their assumptions about consumer spend were far too aggressive.

It happens all the time, especially in strange times like 1Q was, but there's also career/political incentive to be aggressive on the advanced data, since that's what drives the big headlines.

[1]https://www.bea.gov/system/files/gdp1q25-3rd-chart-02.png

By game_the0ry 2025-06-2623:243 reply Given how many layoffs there have been and how much bad economic news has been coming out, I am quit surprised that we are not in a full blown technical recession. Even the DJI is touching historic highs and bond yields are down.

I know I sound like an armchair economist, which is probably why I am on here ranting instead of on a tropical beach with super models name Brooke and Tiffany, eating lobster and beluga caviar, washing it all down with fine champagne.

I can only assume that the last 5 years have been so solid for the economy that we have a long way down to go before we even begin to feel pain.

By toomuchtodo 2025-06-270:34 Structural demographics. ~13k-14k workers leave the labor force every day, through a combination of retirement and death. Beat on the economy hard with these terminal interest rates and tariffs, demand for labor will still exceed supply.

https://hn.algolia.com/?dateRange=all&page=0&prefix=false&qu...

By kylehotchkiss 2025-06-2718:53 I appreciate you named your imaginary supermodels

Recession is when the economy was in decline for three quarters and it were not three quarters yet.

Sorry, but the widely accepted definition of a technical recession is typically identified by two consecutive quarters of negative growth in real gross domestic product (GDP). Tuesday is the cut off date for the quarter and that will determine if the US is in technical recession.

By firesteelrain 2025-06-2721:15 You're right that the textbook definition of a technical recession is two consecutive quarters of negative real GDP growth. That part’s clear.

So technically, we can say “Q2 is over” on Tuesday, but we won’t be able to declare a recession (or not) until that data comes out. Unless you're inside the Fed or BEA models, we're all just speculating until then.

The advance estimate drops on July 22 from the BEA.

US is in a slight slowdown though

{kind=link}