The Iran war is blowing up more than oil refineries

You and I have seen a lot of headlines talking about the Iran war. Most of them have —rightfully — been focused on oil, gas and energy, with some analysts calling it the biggest oil disruption in history.

These are important perspectives that focus on the immediate impacts of the conflict.

But today I want to explore a different question that I haven’t seen others asking.

First, a thought exercise.

What do you think of when you think of Dubai?

Skyscrapers? A highly rated international airport? Toiling migrant workers? Chocolate?

I think of money. More specifically, I think of oil money that became AI money, climate money, real estate money and infrastructure money.

Oil and capital are inextricably connected, and the world runs on both.

So what happens when a war with global potential embroils the region that supplies the world with not just one but two of its most important feedstocks?

The Gulf states that are currently being bombarded by shrapnel matter first because there are people living there, but second because they export not only ⅙ of the world’s portable, storable, energy dense fuels but also the capital that powers our global financial system.

Today, I’m going to argue that this is the sleeper story we’re not paying enough attention to, and I’ll also share a few suggestions for how to navigate this time of extreme volatility and risk.

The news has been all over the oil story. Oil jumped past $100 / barrel for the first time since 2022. The Strait of Hormuz is closed, cutting off the supply chain for 20% of global oil consumption and 20% of global LNG.

Oil producers are cutting or shutting production all over the Gulf region, and it will have knock-on effects on everything from the price of fuel to the price of everyday goods that are grown and/or transported by that fuel to the leverage that Russia has on the war in Ukraine.

The oil story is not minor, but what this war will do to capital could have even longer repercussions.

The single most underreported story of the war in Iran is about an obscure and little used legal escape hatch called force majeure.

I’m not talking about the widespread reporting covering how Gulf region energy companies have been declaring force majeure to get out of shipments and sales contracts. Those are straightforward cases where physical barriers make it impossible for producers to deliver — things like a drone strike on a refinery or the closure of the Strait of Hormuz.

I’m talking about the buried-on-page-12 reporting from The Financial Times that at least three of the four major Gulf economies have started internal reviews to determine whether or not they can invoke force majeure to be released from their investment contracts.

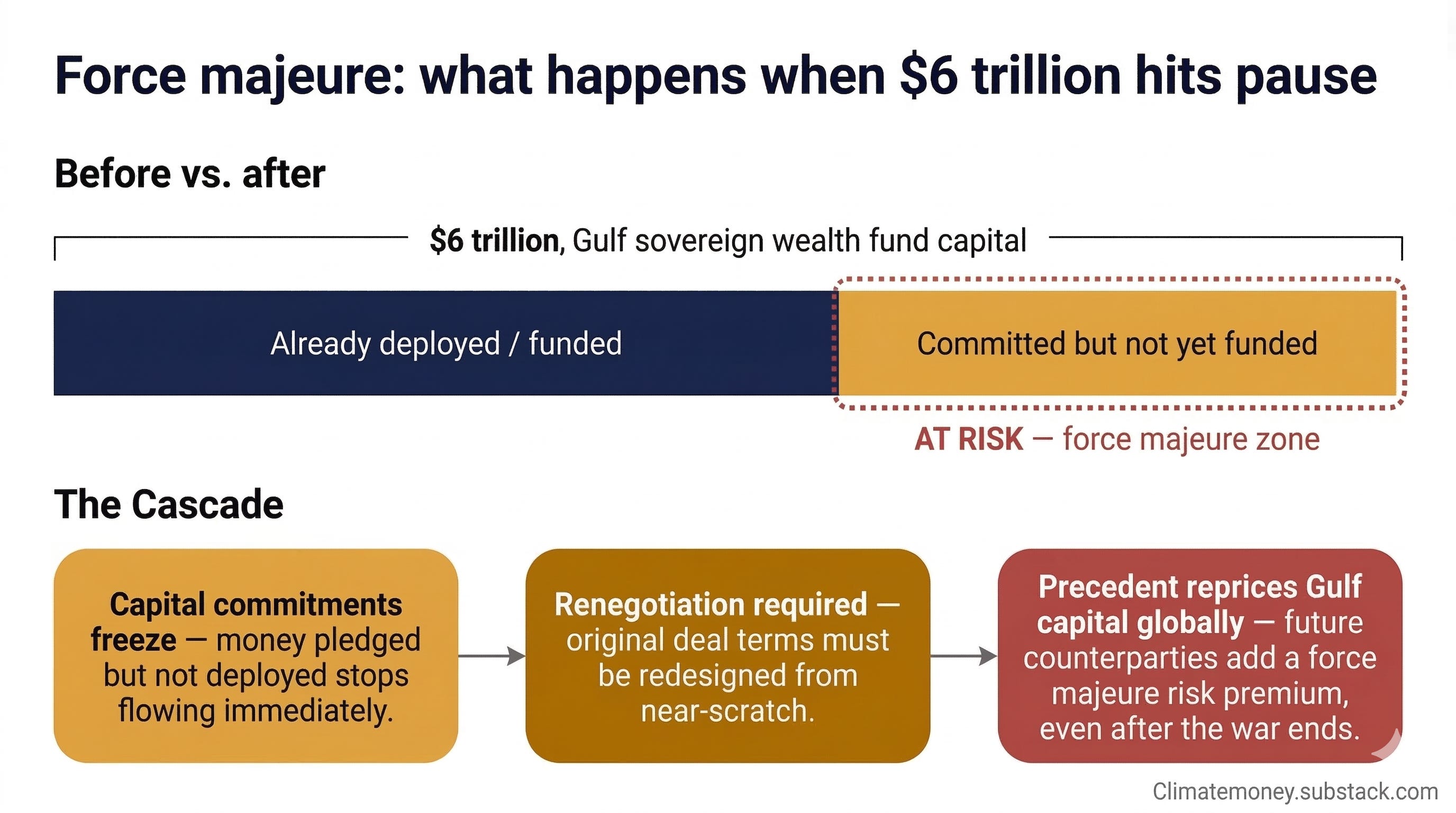

Gulf Cooperation Council sovereign wealth funds collectively manage $6 trillion in global assets. This accounts for over 40% of all sovereign wealth fund capital on Earth. If successful, force majeure would release the world’s biggest investors and creditors from hundreds of billions of dollars in financial obligations that are currently the backbone of the AI boom and the energy transition.

The FT article says the Gulf states are engaging in a “coordinated review” of investment commitments made to:

foreign states and companies

sports sponsorships

contracts with businesses and investors

and they’re also looking into potential sales of holdings.

Force majeure is a clause in contract law that lets a party pause or completely get out of contractual obligations in the face of extraordinary events. Invoking force majeure in sovereign investment agreements would be without modern precedent.

Over the decades, Gulf sovereign wealth funds have seen a lot:

oil price collapses

various regional conflicts

the 2008 financial crisis

COVID

None of these circumstances prompted anyone to start talking about force majeure reviews on US or international investment commitments. Now we know that they’re seriously exploring this — and letting the world know about it.

So what would actually happen if Gulf states invoked force majeure? A few things:

First, it would legally suspend their obligation to fund committed capital — meaning money committed but not yet deployed stops flowing immediately.

Second, even though it doesn’t necessarily mean a permanent exit since force majeure suspends obligations for the duration of the triggering event but doesn’t cancel them, it means that the original commitments would need to be renegotiated or even redesigned once the conflict is over.

Third, we’ll very likely see timelines on dependent projects slip — possibly by 12 to 18 months, possibly into oblivion. More on this below.

If force majeure is successfully implemented, it would also set a precedent that could reprice Gulf capital globally even after the war ends. In other words, it would be riskier and more expensive to accept Gulf state backers in the long run.

All of which adds up to a lot of risk for the Gulf sovereign wealth funds who’ve spent decades carefully building and executing a strategy to turn oil dollars into the capital scaffolding of the future. Why would they do this?

We know that the White House knows about these discussions, even though they haven’t addressed them publicly. There are White House sanctioned projects — like Stargate — that would be squarely in the strike zone if capital gets pulled back. The stated reasoning is that Gulf economies are reassessing capital allocation to address mounting needs on their home turf — defending desalination plants is going to cost some money.

But I think the bigger play here is diplomatic. One of the best ways to extract the behavior you want in a system driven by capital is to threaten to withhold its lifeblood — money.

Even if no one ultimately runs the force majeure play here, knowing that it’s in the cards could be enough to shake the foundations of the confidence game that we call the global financial system.

Imagine you’re a VC fund manager. Despite a challenging market, you’ve managed to secure a solid commitment from a major anchor investor. Thanks to them agreeing to back 25% of your fund, you were subsequently able to close a bunch of other LPs and start backing companies.

Now imagine that your anchor LP is QIA — the Qatari Investment Authority, which with its $557B in assets under management is one of the biggest global sovereign wealth funds and a major investor in countless VC funds, not to mention technology infrastructure, real estate, media companies, hospitals and much more. Under normal circumstances, investors can’t exit their signed investment commitments without incurring major penalties that are specifically designed to prevent them from backing out. But this time, they’ve successfully invoked force majeure and now they’re systematically reevaluating which commitments they’re going to need to “pause” and which ones they can keep.

Is QIA going to sell down their ownership stake in Harrods or Canary Wharf so that they can fund their pledges to your VC fund (or your data center, or your solar array)? It’s impossible for outsiders to guess at what that internal prioritization meeting might look like, but it actually doesn’t even matter. All we need to spook markets — and other investors — is the specter of possibility.

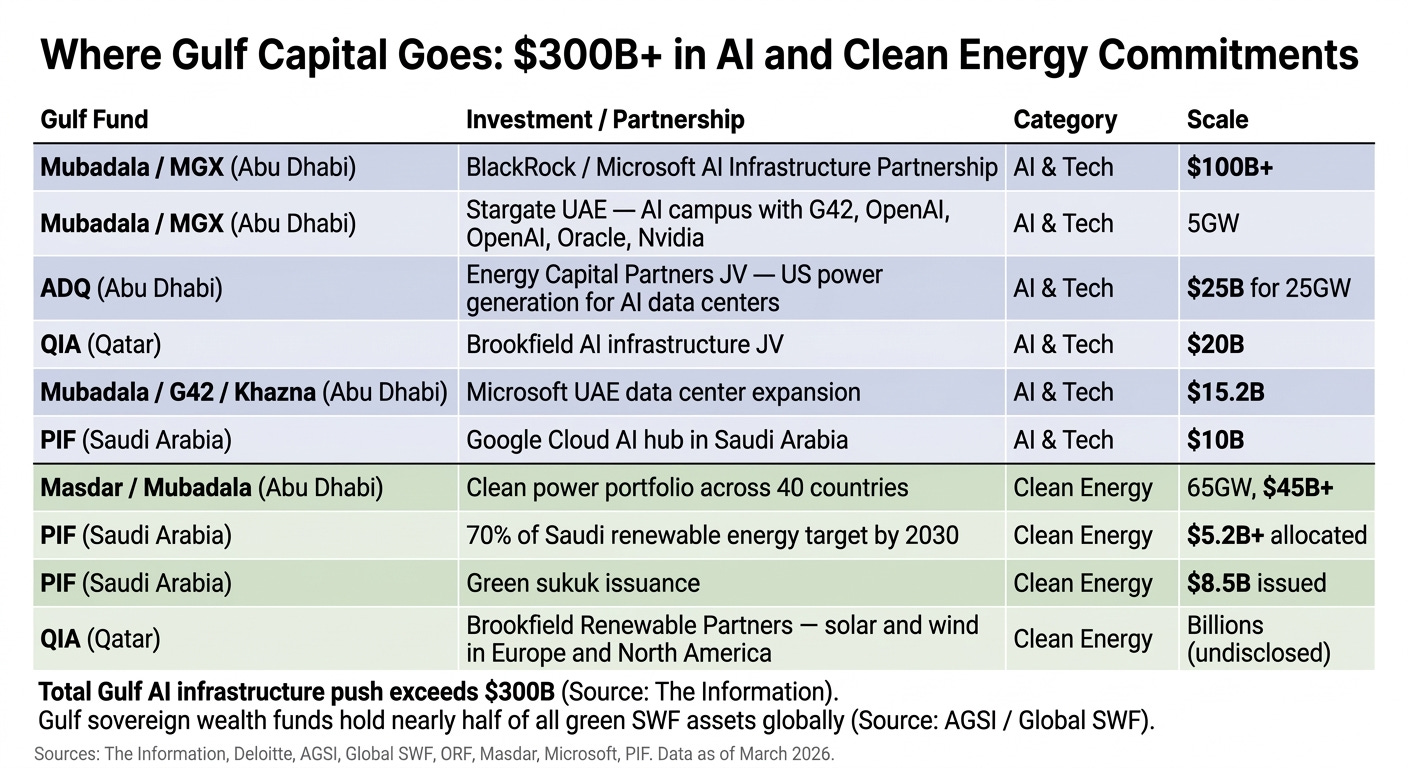

All this feels abstract until we look at where those dollars are actually going. For decades, the Gulf states have been quietly alchemizing petrodollars into the biggest bets for humanity’s future.

In AI, the Gulf sovereign wealth funds are everywhere. We’ve read about that. But do you know how active they are in the climate and energy transition? Half of all green sovereign wealth fund assets around the world are held by Gulf funds.

SWFs like the Public Investment Fund of Saudi Arabia, the Qatari Investment Authority and Mubadala out of Abu Dhabi have collectively put billions of dollars into hundreds of clean gigawatts across dozens of countries around the world, including the US.

Even if you’re not in or adjacent to the world of finance (good for you!) and you couldn’t care less about the 21st century underpinnings of global capitalism, if you’re here at Climate Money you presumably care about the climate and energy transition. The Gulf states have done serious work to drive the energy transition around the world — in their own backyards, but also in emerging markets, the EU, the UK, and right here in the US — and all of that could be pulled back thanks to an opaquely reasoned offensive strike.

I mentioned earlier that force majeure introduces a pause, not an end to capital deployment.

But for many deals, the pause is the end.

For example, in renewables project finance, if your key capital commitment falls through mid-construction, three things happen:

the project’s cost of capital spikes because other lenders reprice risk

contractors and suppliers who were counting on a specific timeline start looking for other work, and

the interconnection queue, permitting timeline, or offtake agreement all could expire.

If a Gulf sovereign wealth fund invokes force majeure on its commitment to Stargate, construction could slip by 12 maybe 18 months. A year in, you don’t pick up where you left off. Chip orders get redirected. Construction crews move on to other contracts. PPAs expire and have to be renegotiated. You’re not ‘merely’ 12 to 18 months behind; you’re looking at starting over.

In project finance, we’re looking at a tight time sequence of interlocking commitments — an intricate dance of documents, deadlines and decision points. (obligatory yet wholly appropriate shout out to my personal heroes at Euclid Power for chipping away at this oft-sloppy complexity!)

Your position in a multi-year interconnection queue, your 6 to 12 month lead times on panels and inverters, your fixed schedule construction financing and your power purchase agreement with a commercial operation date are not independent variables. They’re more like a string of Christmas lights, but the old school kind where one outage means you have to throw out the entire bunch.

Even if you’re able to isolate the damage, the most likely minimum impact is that your project’s cost of capital just spiked as lenders reprice risk and every other participant in your capital stack demands a higher return to compensate them for the uncertainty they’re taking on. More risk, more cost.

A project that used to work at 7% cost of capital now needs 9% or 10%, or maybe doesn’t pencil at all anymore. This is a meaningful threat to the energy transition, especially here in the US where the Trump administration’s recent changes to the regulatory and tax regimes have already made energy transition work more expensive, slower, and less competitive with fossil fuels.

Let’s talk about the ripple effect.

Gulf sovereign wealth funds aren’t isolated actors. They’re embedded in co-investment structures with BlackRock, Brookfield, Microsoft, Google, and dozens of other institutional investors. When an anchor investor goes under review, the entire co-investment ecosystem feels it.

Fund managers could delay capital calls, slow *deployment, or reduce fund sizes. Co-investment partners will be pressed to decide whether to fill the gap with their own balance sheets or slow the deal. Lots will choose to slow the deal.

Secondary market pricing for Gulf-related fund positions could drop, creating mark-to-market losses that cascade through LP portfolios. With some of the world’s biggest LPs preoccupied with war, new fund formation in clean energy and infrastructure gets harder. A lot of climate and energy transition funds I know are fundraising right now, or were about to start. We have tough timing yet again thanks to the White House.

And then we have to talk about the feedback loop. If Gulf renewable projects slow down, that’s less clean energy supply coming online in a region that was supposed to be a major contributor to global decarbonization. Less clean energy supply means more and longer dependence on fossil fuel infrastructure (that’s now under attack btw). Energy prices around the world stay high or get higher, and that will have knock-on effects for everything from heat pumps in California to the emissions trading system in Europe to EVs in China.

But you knew that already, didn’t you?

Still, I’ve seen commentators putting forth variations of “this war will be good for renewables because oil and gas will be bottlenecked.”

In reality, wars crush infrastructure, destroy capital, redirect government spending to defense, disrupt supply chains and aggregate political will around the shortest term solutions. Contrary to some ‘copium’ takes from the climate transition world, elevated energy prices do not immediately increase incentive to adopt renewables; they reduce the economic buffer that enables governments to go long on energy transition. (However, the idea of renewables as defense and deterrence is something we should be thinking harder about…)

Look, there are kids being bombed, wild animals being incinerated in drone fire, fossil fuels filling the air and water in a region of over 60 million people. So what can we do?

The honest answer is not much. But that’s never stopped me from worrying and trying.

I racked my brain for different things I could say here, because I don’t like to end posts with a shrug and a prayer. The one phrase that kept popping into my mind — possibly due to my lifelong affinity for my AP US history textbook — was “victory garden.”

During WWII, American civilians were told that they couldn’t control the war, but they could grow their own victory garden — some vegetables in a backyard plot or balcony. No one was feeding a family of four on backyard carrots, but that wasn’t the point. Instead, it gave people a lever they could lean on — a sense of action, and perhaps, satisfaction in a time of great unease. Maybe it slightly reduced supply chain pressures during an all-hands-on-deck global situation. Maybe it didn’t.

But in times of great, flattening global crisis, the two best things you can do are to build autonomy, and to diversify.

If you’re an investor or allocator — the projects most at risk right now are in the committed but not funded stage. If you’re tracking infrastructure or clean energy deals with Gulf capital in the stack, check whether funding has actually been drawn or is still at the commitment stage. Build liquidity buffers and diversify your LP exposure.

If you’re a founder or operator in climate — your supply chain assumptions just changed. If you’re raising capital, understand that new money may slow for 6 to 12 months or more. Diversify your investor base. If you’re in project finance, watch for rising insurance costs because reinsurers are global.

If you’re just a person — energy prices are going up and will probably stay there for awhile. Energy resilience via a rooftop solar system, a heat pump and/or an EV are hedges in a world where the price of energy can be set by what’s happening in a war none of us asked for.

One of the biggest frustrations that small children and elder adults share is their lack or loss of agency.

I’ve been thinking a lot about this a lot lately as my own kids are still small but vocal, and my parents are forced to contain their rich desires within their aging bodies. Everyone wants sovereignty, but none of us have it completely.

We’ve talked about how the global financial system is an intricate web of interlocking commitments. You can’t pull its biggest threads without unraveling something three continents away.

The flip side of this is that every node matters. The interconnectedness that makes the system fragile also means that every individual action is significant.

Victory gardens didn’t end World War II. But a million little gardens, in aggregate, freed up some capacity in a supply chain under siege. They also engaged Americans in micro actions that led to bigger participation, the ultimately antidote to apathy.

The climate transition is in the same place right now. We need a hundred million acts of micro resilience at the household level, the portfolio level, and the policy level. We need to leverage independence to build up interdependence. And we need the wars to stop.

Read the original article

Comments

By aurareturn 2026-03-1221:29

I might be living under a rock but everyone is talking about the GCC's capital.Today, I’m going to argue that this is the sleeper story we’re not paying enough attention to, and I’ll also share a few suggestions for how to navigate this time of extreme volatility and risk.The core of Iran's strategy is to hurt the GCC financially which hurts the US financially. This is literally THE story. It's not the sleeper story. It's the main story and why stocks have been swinging like crazy.